Buying a home in Nepal is a dream for many, whether you are a first-time buyer or a Non-Resident Nepali (NRN) looking to invest back home. Despite banks offering attractive single-digit home loan rates ranging from 5.96% to 10.50%, the growth in housing loans has slowed to just 4.07% over the past year. This indicates that while loans are financially appealing, many buyers remain cautious due to weak consumer confidence or challenges in qualifying for a loan.

Navigating the home loan process in Nepal can be challenging without proper guidance. From understanding eligibility criteria to selecting the right type of loan and completing the application process, each step requires careful attention. First-time buyers can take advantage of increased loan-to-value ratios (up to 80%) and special schemes for NRNs, making this a potentially favorable time to enter the property market.

In this article, we will walk you through every stage of the home loan journey in Nepal, highlighting key considerations for first-time buyers and NRNs alike. By the end, you’ll have a clear roadmap to secure a home loan confidently and efficiently.

Overview of the Real Estate Market in Nepal

Nepal’s real estate market has been steadily growing, especially in urban centers like Kathmandu Valley, Lalitpur, and Bhaktapur. The demand for residential properties continues to rise, fueled by rapid urbanization, NRN investments, and government initiatives promoting housing projects.

According to Nepal Rastra Bank, housing loans remain one of the most popular banking products in the country. This trend reflects the increasing interest among Nepalis in owning property as both a necessity and an investment.

For first-time buyers, understanding the financial and legal aspects of purchasing property is essential. NRNs, on the other hand, must also navigate additional documentation and legal requirements, making knowledge about home loans even more important.

Importance of Understanding Home Loans Before Buying a Property

A home loan is often the largest financial commitment most buyers make in their lifetime. Without a proper understanding, buyers risk facing high-interest rates, unexpected fees, or eligibility issues. Key benefits of understanding the home loan process include:

- Financial Planning: Know your budget and repayment capacity.

- Time Efficiency: Avoid delays in approval and disbursement.

- Informed Decisions: Select the most suitable loan type and lender.

- NRN Advantages: Learn specific loan options and exemptions available to NRNs.

Nepali citizens below 65 years of age who are eligible to obtain a home loan for the construction of a residential house on a plot of land located within the institution’s designated operational area.

Loan Eligibility Criteria By ADBL Bank:

- A valid house construction permit must be obtained from the appropriate regulatory authority.

- Construction must have progressed at least up to the Plinth Level ( DPC).

- The house to be constructed, extended, or renovated must be accessible via a road with a minimum width of 10 feet.

Loan Amount, Tenure, and Type:

- Financing is available for up to 70% of the total cost of construction, extension, or renovation, based on a cost estimate prepared by an engineer registered with the Nepal Engineering Council.

- Loan tenure options:

- Up to 5, 10, or 15 years for house construction.

- Up to 3 years for house renovation.

- The home loan will be non-revolving in nature.

Minimum Income Requirements

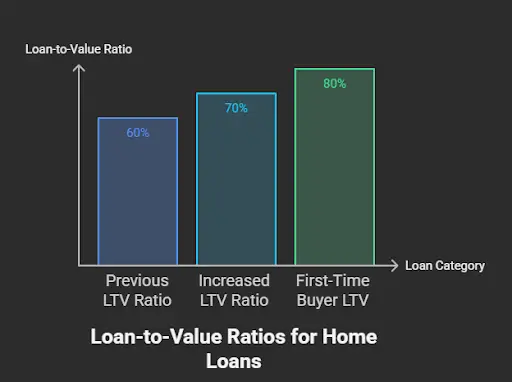

Banks assess your monthly income to determine loan eligibility. Salaried employees, self-employed professionals, and NRNs need to provide proof of stable income. With the recent increase in loan-to-value (LTV) ratios from 60% to 70%, and up to 80% for first-time buyers, individuals with moderate incomes can now qualify for larger loans, making home ownership more accessible (NEPSE Trading, Rising Nepal).

Credit History and Financial Stability

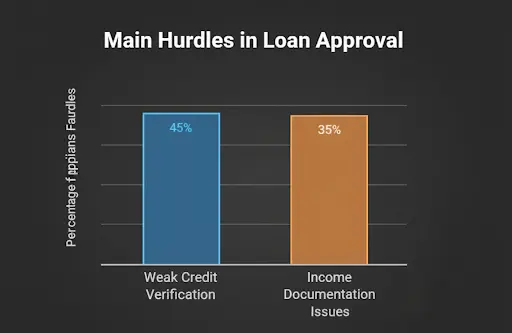

A good credit score is crucial. Banks evaluate past loans, repayment behavior, and overall financial stability to minimize risks. Despite banks offering single-digit interest rates (5.96% – 10.50%), many borrowers face challenges due to weak credit verification and income documentation, which remain key hurdles in the approval process (The Annapurna Express, Rising Nepal).

NRN-Specific Rules

NRNs must comply with legal regulations, including providing Nepalese citizenship proof, NRN status verification, and repatriation plans for loan repayment. Some banks also offer special loan schemes exclusively for NRNs.

Types of Home Loans Available

Understanding the different types of home loans in Nepal helps buyers choose the option that best fits their financial situation and long-term plans. Banks in Nepal now offer a variety of loan products, some specifically tailored for NRNs, first-time buyers, and environmentally conscious homeowners.

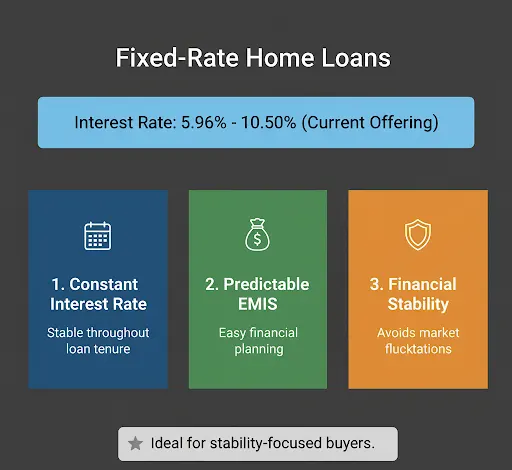

Fixed-Rate Home Loans

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Ut elit tellus, luctus nec ullamcorper mattis, pulvinar dapibus leo.

- Interest rates remain constant throughout the loan tenure, providing predictable EMIs for better financial planning.

- With current offerings, fixed rates range from 5.96% to 10.50%, depending on the bank (Insurance Khabar).

- Ideal for buyers who want stability and want to avoid fluctuations in monthly payments.

Variable-Rate Home Loans

- Interest rates fluctuate based on market conditions, usually tied to the base rate or repo rate set by Nepal Rastra Bank.

- Can be beneficial if rates decrease over time, but carry the risk of rising EMIs.

- Banks like Agricultural Development Bank, Everest Bank, and Rastriya Banijya Bank provide competitive variable-rate options (Insurance Khabar).

Special Loans for NRNs or Government Employees

- NRNs can access tailored schemes with favorable interest rates, extended repayment periods, and flexible remittance options (NEPSE Trading).

- First-time homebuyers benefit from increased LTV ratios (up to 80%), making it easier to finance their first property purchase (Rising Nepal).

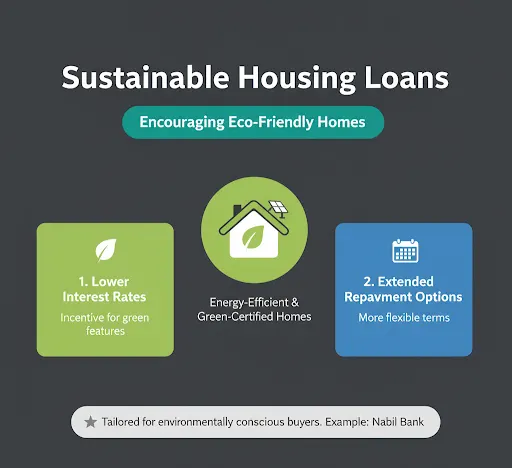

Sustainable Housing Loans

- Some banks, such as Nabil Bank, have launched sustainable housing loans to encourage environmentally friendly home construction (Kathmandu Post).

- These loans may offer incentives, such as lower interest rates or extended repayment options, for energy-efficient and green-certified homes.

Tip for Buyers: Compare multiple banks for interest rates, loan terms, and additional benefits before applying. Consider your long-term financial stability and repayment capacity when choosing between fixed, variable, or special loan schemes.

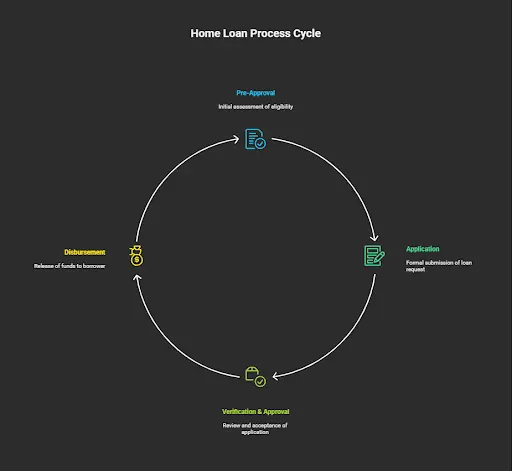

Step-by-Step Home Loan Process

Navigating the home loan process in Nepal requires careful attention to each stage. Below is a detailed, step-by-step guide incorporating current banking practices, policies, and recent updates that make the process smoother for buyers, especially first-time buyers and NRNs.

a. Pre-Approval

Assessing Loan Eligibility:

- Banks evaluate your monthly income, credit history, and financial stability to determine the maximum loan you can secure (The Annapurna Express, Rising Nepal).

- NRNs may need to provide additional documents, such as citizenship proof, NRN verification, and remittance plans (NEPSE Trading).

Documents Required:

- Citizenship or passport (for NRNs)

- Proof of income (salary slips, tax returns, or bank statements)

- Property documents (sale agreement, land registration certificates)

- Any additional documentation required by the bank based on loan type

b. Application Submission

Filling Out the Application Form:

- Submit a complete and accurate loan application. Errors or missing details can delay approval.

Attaching Necessary Documents:

- Attach all supporting documents, including identification, income proof, and property documents.

- Ensure LTV compliance: up to 80% for first-time homebuyers and 70% for other buyers (NEPSE Trading).

c. Loan Verification & Approval

Bank Verification Process:

- The bank conducts an assessment of the borrower’s financial and credit history.

- NRNs may face additional verification steps due to remittance tracking.

Property Appraisal:

- Banks require a certified property valuation to confirm the market price of the home.

Credit Check:

- Banks review past loans and repayment behavior to assess risk.

- Even with single-digit interest rates (5.96%–10.50%), weak credit history can delay or block approval (Insurance Khabar).

d. Loan Disbursement

Signing Agreements:

- Review the loan contract thoroughly, including interest rates, EMI schedules, and repayment terms.

Fund Release Process:

- Once approved, the bank disburses the loan directly to the seller or developer.

- Standard timelines: 2–4 weeks after document verification and property appraisal (Industry estimate).

Additional Notes:

- For loans in earthquake-affected areas, rescheduling is possible by paying a minimum 10% interest (NEPSE Trading).

- Sustainable housing loans may have specific disbursement conditions if building a green-certified home (Kathmandu Post).

Tip for Buyers:

- Start the process early and maintain organized documentation.

- Compare banks for interest rates, processing fees, and special schemes to maximize benefits.

Tips for a Smooth Home Loan Process

Securing a home loan in Nepal can be a seamless experience if you follow these actionable tips, especially given the current banking landscape and policy updates:

- Prepare All Documents in Advance

- Keep identification documents (Citizenship or Passport), income proof, bank statements, and property documents ready.

- NRNs should ensure that the NRN verification and remittance documentation is complete (NEPSE Trading).

- Keep identification documents (Citizenship or Passport), income proof, bank statements, and property documents ready.

- Compare Interest Rates Across Banks

- Single-digit home loan rates are now available across banks, ranging from 5.96% to 10.50% (Insurance Khabar).

- Compare rates for fixed, variable, and special NRN loans to choose the most cost-effective option.

- Single-digit home loan rates are now available across banks, ranging from 5.96% to 10.50% (Insurance Khabar).

- Understand LTV and Loan Limits

- Maximum LTV ratios have been increased to 70% for general buyers and 80% for first-time buyers (NEPSE Trading).

- General home loan limits have been raised from NPR 2 crore to NPR 3 crore, making higher-value properties more accessible (NEPSE Trading).

- Maximum LTV ratios have been increased to 70% for general buyers and 80% for first-time buyers (NEPSE Trading).

- Work with Trusted Real Estate Agents or Financial Advisors

- Expert guidance ensures all documentation is correct and helps you select the right property and loan type.

- Advisors can also help NRNs navigate legal and repatriation requirements.

- Expert guidance ensures all documentation is correct and helps you select the right property and loan type.

- Leverage Special Loan Programs

- Banks like Nabil Bank offer sustainable housing loans for eco-friendly constructions (Kathmandu Post).

- First-time homebuyers can take advantage of higher LTV ratios and flexible repayment schemes to reduce upfront costs.

- Banks like Nabil Bank offer sustainable housing loans for eco-friendly constructions (Kathmandu Post).

- Monitor Bank Timelines and Policies

- Typical loan processing and fund release takes 2–4 weeks after verification (Industry estimate).

- Typical loan processing and fund release takes 2–4 weeks after verification (Industry estimate).

In earthquake-affected areas, loans can be rescheduled by paying a minimum 10% interest (NEPSE Trading).

Conclusion

Securing a home loan in Nepal has never been more accessible, thanks to the recent banking policies, increased loan limits, and attractive single-digit interest rates. With rates ranging from 5.96% to 10.50% (Insurance Khabar) and loan-to-value ratios increased to 70% for general buyers and 80% for first-time buyers (NEPSE Trading), buyers now have more opportunities to invest in their dream home.

Even though the growth in housing loans has been relatively modest at 4.07% over the past year (The Annapurna Express, Rising Nepal), these developments highlight that the market is favorable for informed and prepared buyers, including first-time homeowners and NRNs. By understanding the eligibility criteria, types of loans, and step-by-step process, and by working with trusted real estate agents or financial advisors, you can navigate the home loan process confidently and efficiently.

Additionally, innovative products like sustainable housing loans from Nabil Bank (Kathmandu Post) encourage eco-friendly property development, giving buyers further options to customize their investments.

Start your home buying journey today! Explore properties and get expert guidance at PunarvaasuNepal, and take advantage of the latest policies to make your dream of owning a home in Nepal a reality.